An Advisor's Perspective - Creative Strategies for Long-Term Care Insurance Sales

You are probably aware that Washington implemented WA Cares, the first mandatory state long-term care (LTC) program, in 2021. As a reminder, it is funded by a payroll tax on Washington workers' gross wages, without a cap on their contribution to the program. The lifetime LTC benefit amount is currently $36,500 and it may be indexed for inflation.

Those who purchased a qualified long-term care product prior to November 1, 2021 were able to request a lifetime exemption from WA Cares and its payroll tax. The one-time exemption window is closed and Washington workers can no longer opt out of WA Cares.

With the 2024 elections behind us, we're seeing activity at the state level to address this big financing issue. Many states are currently exploring the feasibility and financing of public LTC programs including California, Connecticut, Hawaii, Kentucky, Massachusetts, Maryland, Minnesota, New York and Pennsylvania.

The Status of Future LTC Initiatives

The long-term care funding problem is not going away. Just as financial professionals must help their clients to be prepared to pay for long-term care costs, states too need a plan. Ultimately, if a resident does not plan for long-term care, the state and federal government end up being the primary payors through Medicaid. As America continues to age, it is likely we will see more states searching for ways to address long-term care needs and reduce their Medicaid expenditures.

While some are looking to WA Cares for inspiration, lawmakers are also considering other options to encourage the purchase of private insurance. For example, one suggested approach in California, after a state program has been implemented, is a reduced payroll tax when workers purchase their own qualifying long-term care insurance policy.

As a financial services professional, what can you do to help? Proactive discussions around long-term care must take place when clients are young and healthy enough to consider alternative plans. Regardless of the potential for future government-sponsored LTC programs, when clients do not have a plan for long-term care costs, their family is exposed to the burdens of informal caregiving, and their financial portfolios can be disrupted to pay for long-term care.

What You Can Offer Clients Now

With an aging population, rising care costs, and financial strain on government programs, the awareness of the need to plan for long-term care is higher than ever. The advisor or financial professional should discuss the expensive nature of self-funded long-term care and the importance of incorporating a solution into financial planning. Instead of relying on self-funding as the default course of action, it's crucial to explore the various options available to cover LTC costs.

The good news, and also the challenging news, is that there are numerous insurance products with medical underwriting that can help cover these costs. Currently, there are eight different forms of LTC solutions available:

- Traditional Long-Term Care Insurance

- Short Term Care Plans (STC)

- Hybrid Life Insurance with LTC Insurance

- Hybrid Annuities with LTC Insurance

- Medically underwritten Immediate Annuities

- LTC Rider on Permanent Life Insurance products

- Life Insurance with a Chronic Illness Rider (upfront charge)

- Life Insurance with a Chronic Illness Rider (charge/benefit determined at time of claim)

It may seem overwhelming to sort through all of these options, so we recommend that you group the decision-making process for LTC insurance into three primary areas:

- Health underwriting considerations

- Long-term care insurance product features

- Funding strategies

Each of these areas can help narrow down the types of plans that should be focused on.

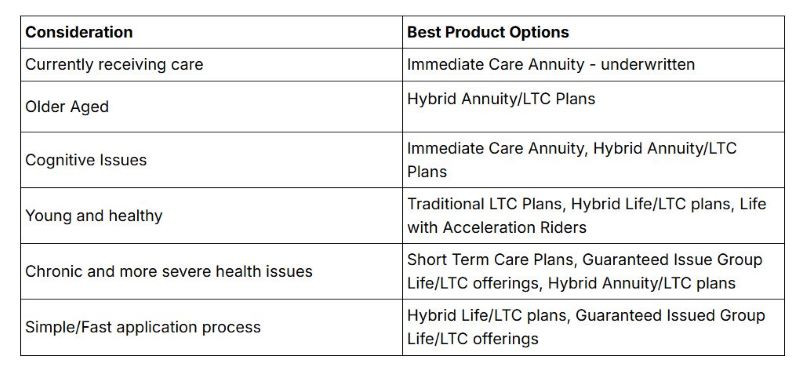

Health Underwriting

What all these options have in common is the requirement for medical underwriting. Unless you're part of a company that offers long-term care insurance with guaranteed issue during an enrollment period, assessing the prospect or client's health should be the initial step in any planning process. The good news is that it's now easier than ever with the availability of online health screening tools.

Once preliminary health information is gathered, certain types of LTC policies are likely to be the best fit based on that information. This doesn't mean that other solutions won't work for a particular person, but it does help narrow down the choices.

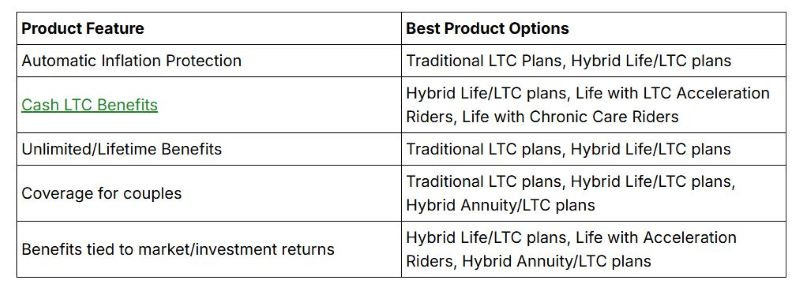

Product Features and Benefits

Once underwriting has narrowed the choice, the next area to consider is LTC product features. Marketplace competition has led to many product features, and asking about ones that clients might be interested in makes sense. Here are some product features and the types of products that might be appropriate:

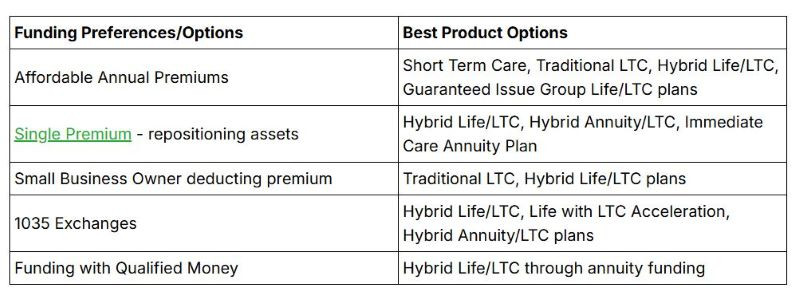

Funding the Plan

Lastly, consideration has to be made on how to fund the LTC plan. Just as the default of self-funding a LTC plan can be subject to liquidity and market timing issues, a plan can be impacted greatly by how premiums are paid. This is where financial advisors and financial services professionals can really help the prospect with some creative ideas. Here are some methods for paying for coverage and which products might be a better fit:

Once you've explored underwriting, product features and funding it should be clear which type of product will be most appropriate. The next step is to look at the possible carriers and filter them based on buyer preferences — for example, "Hybrid Life/LTC carriers that offer unlimited benefits with annual premiums."

Your final task should be to summarize the planning preferences to demonstrate that a best-interest effort has been made. With that done, you can make a suitable recommendation - narrowing down the decision for the client to at most two recommended solutions.

Help On the Process - From People and Technology

For those advisors and financial services professionals who don't work daily on long-term care planning, outside help is a must. That could be in the form of carrier wholesalers and brokerage general agencies who specialize in LTC planning. They can assist with narrowing down the choices and even help with point of sale presentations - which today are primarily done through video conferences.

In addition, insurance technology vendors (like Ensight) are working hard on creating comparison software and illustration tools that allow for interactive comparisons so that variables like premiums or LTC benefits can be tweaked. Carriers and vendors are also creating companions to illustrations that are more focused on stories.

AI Will Help as Well

The hype of AI may be overblown - but make no mistake: it will greatly impact LTC planning. No, it won't replace humans for a while, but as AI is integrated into planning it will make the process of securing LTC coverage more efficient.

Surprisingly, many of the AI tools do know a lot about LTC Insurance — but often their advice is incomplete, misstated, suspect or just simply wrong. As AI learns it should become more reliable over time, but today AI "advice" on LTC should always be scrutinized and verified using authoritative sources.

Conclusion - Don't Let the Choices Overwhelm You - and Don't Let 'Perfect' be the Enemy of 'Good Enough'

We don't know what the future will bring and no LTC plan can be iron clad. The key is to put a plan in place and then monitor it on a periodic basis. LTC offers great opportunities to stay in touch with your clients, and to cultivate additional business through your clients' relationships. Remember, with your help, everyone can make a plan for long-term care.

Windsor wishes to extend our thanks to guest author Tom Riekse Jr, Managing Director of LTCI Partners. As the Managing Director of LTCI Partners, Tom leads one of the largest national insurance distributors focused exclusively on long-term care planning.

Our thanks also to John Hancock's November 2024 Advanced Sales bulletin titled "The votes are in – and it's WA Cares with the win," for contributing much of the material in the opening paragraphs of this Blog.

Additional Resources:

CareScout: Calculate the Cost of Long-Term Care Near You

Stand Alone Long-Term Care Product Comparison (LTCI Partners)

Hybrid/Asset Based Long-Term Care Product Comparison (LTCI Partners)

Comments