The Major Leading Causes of Death: Challenges and Opportunities Affecting the Life Insurance Industry

Understanding the primary causes of mortality in the United States is crucial for several reasons, particularly concerning individual well-being and life insurance mortality. It's equally important to grasp the variables influencing mortality trends and what we might anticipate in the future, as these factors may significantly impact underwriting guidelines and policy pricing.

Below is a summary of the main causes of death in the US as of 2023, accompanied by explanations of each cause. Additionally, there is a discussion about the "headwinds and tailwinds" faced by the life insurance industry today that may impact future underwriting and mortality.

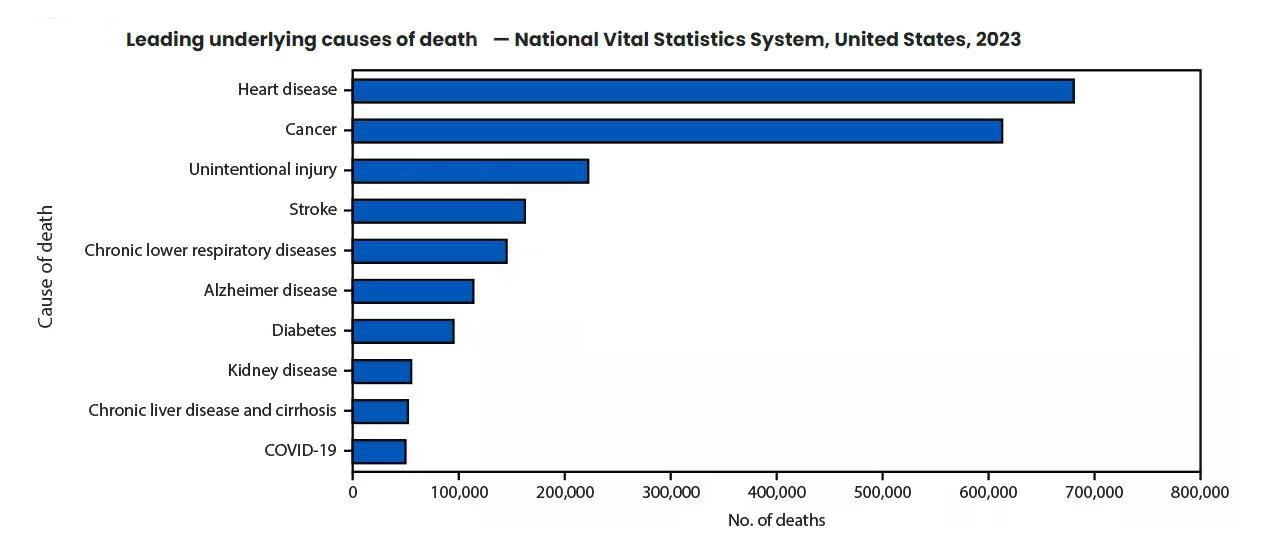

The top 10 causes of death1 include:

- Heart Disease Heart disease remains the leading cause of death in the US, accounting for approximately 703,000 deaths in 2023. This category includes conditions such as coronary artery disease, heart attacks, and congestive heart failure.

- Cancer Cancer is the second leading cause of death, with around 608,000 deaths. This includes various types of cancer such as lung, breast, prostate, and colorectal cancer.

- Unintentional Injuries Unintentional injuries, including car accidents, falls, and drug overdoses, resulted in 227,039 deaths. This category highlights the importance of safety measures and preventive strategies.

- Stroke (Cerebrovascular Diseases) Stroke, or cerebrovascular diseases, accounted for 165,393 deaths. Strokes occur when the blood supply to part of the brain is interrupted or reduced, preventing brain tissue from getting oxygen and nutrients.

- Chronic Lower Respiratory Diseases Chronic lower respiratory diseases, such as chronic obstructive pulmonary disease (COPD) and emphysema, caused 147,382 deaths. Smoking is a major risk factor for these conditions.

- Alzheimer's Disease Alzheimer's disease, a progressive neurological disorder, led to 120,122 deaths. This disease affects memory, thinking, and behavior, and is the most common cause of dementia.

- Diabetes Diabetes caused 101,209 deaths. This chronic condition affects how the body turns food into energy and can lead to serious health complications if not managed properly.

- Nephritis, Nephrotic Syndrome, and Nephrosis Kidney diseases, including nephritis, nephrotic syndrome, and nephrosis, caused 57,937 deaths. These conditions affect the kidneys' ability to filter waste from the blood.

- Chronic Liver Disease and Cirrhosis Chronic liver disease and cirrhosis resulted in 54,803 deaths. These conditions are often caused by long-term damage to the liver from factors such as alcohol abuse and hepatitis.

- COVID-19 COVID-19, which was the fourth leading cause of death in 2022, became the tenth leading cause in 2023, with 49,932 deaths2. The significant decrease in deaths from COVID-19 reflects the impact of vaccination, herd immunity, and other public health measures.

In their "RGA Speaks Volumes" webinar3, Daniel Brand, VP & Actuary, Experience Studies & Analytics, USIL Actuarial, and Daniel Zimmerman, MD, SVP, Chief Science Advisor & Managing Director, Longer Life Foundation, discussed several of these causes of death, specifically as they relate to mortality "headwinds and tailwinds" impacting life insurance underwriting and pricing today.

As they discussed, heart disease and cancer have been the top two causes of death in the US and globally since the mid-20th century. While we've seen remarkable advancements in diagnosing and treating these and other diseases, progress has slowed regarding some medical conditions for various reasons. Life mortality headwinds include:

- Slower cardiovascular improvement compared to past trends

- Obesity and physical inactivity which are major drivers of diabetes and cancer

- Cognitive/neurodegenerative diseases, particularly among older adults

- Infectious diseases, such as COVID-19, flu, and other viruses new to humans

- Economic and demographic factors, such as declining birth rates and an aging population

- Climate change and environmental issues

- Substance abuse, including alcohol, drugs, opioids, and vaping

- Alcohol abuse, accidental overdose and suicide due to social and/or economic circumstances

- Public health access/issues

At the same time, there are several positive tailwinds that could promote better health and improved mortality in the future. These include:

- Genetic discoveries and treatment

- Precision medicine, next-generation cardiovascular therapies, and biometric monitoring

- New obesity and diabetes treatments, like GLP-1 RA (Wegovy, Ozempic, and others) medication

- Improved cancer prevention and screening, early multi-cancer detection, personalized treatment, and recurrence surveillance

- mRNA technology and universal vaccines, including influenza vaccines

- Artificial Intelligence/GTP, machine learning for clinical use and research

- Advanced therapeutics, Artificial Intelligence driven drug and protein development, Alzheimer's disease prevention/treatment

- Microbiome research, focusing on the collection of microbes living on or inside the body

- Regenerative medicine and xenotransplantation

- Anti-aging therapies

As with many medical conditions, diagnosis, prevention, and screening are key. Achieving the best underwriting outcomes requires prompt preventive measures and treatment to address the problem at hand before it escalates. For potential heart disease, this might involve managing cholesterol to slow coronary artery plaque development, maintaining a healthy body weight, and controlling blood pressure. If there is a family history of early-onset heart disease, a stress echocardiogram may be useful for ruling out cardiac issues. Regarding cancer prevention, regular screenings, such as colonoscopies, mammograms, and PSA tests, are very beneficial.

Additionally, a company whose mission is to detect cancer early, GRAIL, has developed a blood test capable of detecting over 50 types of cancer from just a few vials of blood. Life industry leaders, including Windsor's Marc Schwartz, are advocating this test4, which shows promise in detecting cancer at its earliest stages before clear symptoms arise, potentially leading to better outcomes and cures. [View a short video on GRAIL here]

Although many variables influence mortality rates, trends typically develop over extended periods. Apart from uncommon events like COVID-19, life insurance mortality changes gradually. As Brand and Zimmerman emphasize, predicting mortality is intricate and requires specialized expertise. We will have to observe how these and other future impacts on mortality may affect underwriting and policy pricing.

Notes:

1All listed mortality statistics other than COVID-19: FastStats - Leading Causes of Death (cdc.gov)

2Mortality in the United States — Provisional Data, 2023 | MMWR (cdc.gov)

3"RGA Speaks Volumes" webinar, Tuesday July 18, 2023, Today's Mortality Headwinds & Tailwinds, Daniel Brand, VP & Actuary, Experience Studies & Analytics, USIL Actuarial, and Daniel Zimmerman, MD, SVP, Chief Science Advisor & Managing Director, Longer Life Foundation,

Comments