How to save $5 billion for retirement in a fully non-taxable qualified plan

We're guessing that Roth IRAs probably don't show up on your radar these days. What with the S&P, NASDAQ and the Dow ringing the bell on new records almost weekly, investment advisors focused on wealth creation might just pass right by a qualified plan option with income ceilings of about $200,000 and contribution limits of $6,000 to $7,000 (depending on age) annually, as of 2021.

But Peter Thiel of PayPal fame might change your mind. He simply used a Roth IRA to create a $5 billion tax-exempt fortune.

Roth IRAs were created in 1997 to provide for a need not filled by other qualified plans – an opportunity to put after-tax dollars into a financial instrument designed to provide both tax-exempt asset growth and tax-free income for retirement. In 1999, Thiel saw an opportunity to take advantage of the Roth IRA rules in a big way: he contributed $1,664 to his Roth and used that money to purchase 1.7 million shares of his startup, PayPal, for $0.001 per share. How could he do that? The shares were pre-IPO, so there was no ascertainable public value for the shares: they were worth what Thiel said they were worth.

By the time eBay purchased PayPal three years later, the IRA-held shares were worth $28.5 million. Thiel used those proceeds to make other investments, including a $500,000 stake in Facebook in 2004. You can fill in the rest.

Unfortunately, it's unlikely that the opportunity to purchase pre-IPO shares of a company like PayPal will come your client's way any time soon. But recently the Wall Street Journal ran an article titled "A Little-Known 'Back Door' Trick for Boosting Your Roth Contributions." The strategy hinges on a seldom-used contribution rule of 401(k) plans that allows for additional after-tax employee contributions to the plan. That rule increases the maximum total 401(k) contribution allowed from $19,500 to $58,000 for employees under age 50. After making such contributions, the article suggests that the after-tax funds be rolled into either a Roth IRA or a Roth 401(k) where investment growth and eventual retirement income will be exempt from income taxes. According to the article, "You could really see your Roth IRA grow exponentially this way. The best place retirement money can end up is in a Roth account, where it grows totally tax-free for the rest of our lives."

The Journal calls this a "back-door mega strategy." But what's the catch? We asked our friend Joel Shapiro at NFP Retirement to review the WSJ article and let us know what he thought. "Backdoor Roth is certainly an available design option for companies sponsoring 401(k) plans," replied Joel. "They do offer the ability to pump more money into the plan and reap the benefits of Roth tax treatment. The major hurdle is that it isn't as easy to max out the 415 annual additions limit as most articles seem to indicate. First, plans need to be amended to allow for after-tax contributions, allow for Roth, and allow for conversion of same. That's all simple enough. Next participants have to realize, these after-tax contributions are neither Roth contributions nor traditional pretax deferrals (both of which have to be aggregated for 402(g) limits). They are entirely additional contributions.

"The hitch? After-tax contributions have to be included in a plan's actual contribution percentage (ACP) testing (most plan sponsors are familiar with the ACP test conducted for their matching contributions). And unless the plan has a lot of non-highly compensated employees (NHCE) that are willing to pump in after-tax contributions, there will be some pretty low limits placed on the amount of after-tax contributions that can actually be made and then converted to Roth by highly compensated employees (HCEs). And when you think about it pragmatically, how many NHCEs are likely going to max out their pretax deferrals/Roth up to the 402(g) limit and then defer even more of their compensation into the plan in after-tax contributions to loosen up the limits to allow HCEs to take full advantage of the backdoor Roth? Generally not many. So while the option is available for companies to consider offering, the reality is that each company should probably review their plan demographics to determine if the juice will even be worth the squeeze."

Taking it all together, the "mega-strategy" could offer some lift to your clients' retirement plans, but it's not for everyone — and the stars have to align correctly to make it work. Still, the advantages to a "back-door" IRA are hard to ignore:

- After-tax contributions allowed of almost $40,000 annually

- Tax-exempt investment growth

- Tax-free distributions for retirement

- Minimal limitations – Penalty-free distributions from age 59 ½; plan must be at least 5 years old

- No RMDs; no capital gains tax

If only there were another way.

How About a "Front-Door" Life Insurance Retirement Plan?

If going around to the "back door" won't work for your client, we suggest that you try a more direct approach. Cash value life insurance, in all of its various forms, has the advantages of a "back door" Roth IRA already built in:

- Tax-deferred investment growth; potentially tax-exempt life insurance element

- Tax-free distributions for retirement using withdrawals and policy loans

- Penalty free distributions at any time

- No RMDs; no capital gains tax

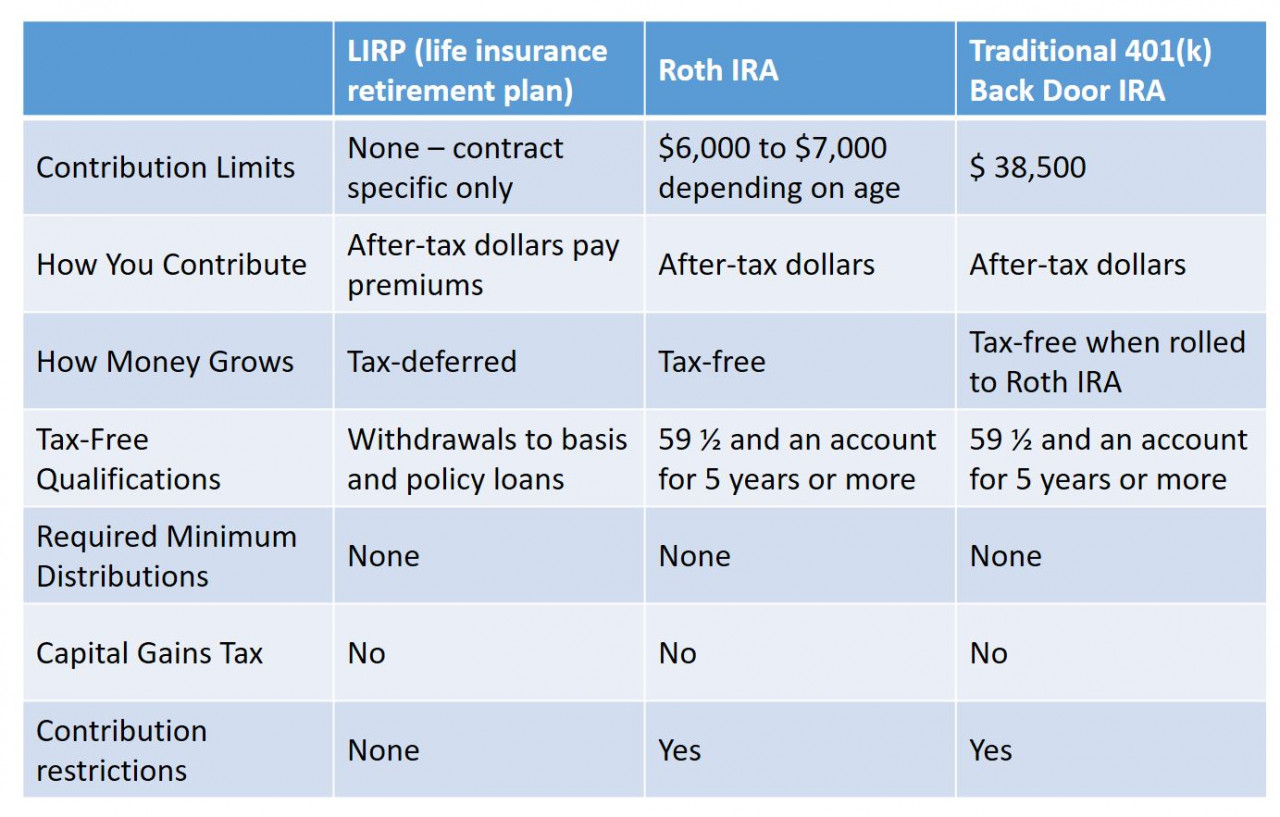

As you can see, a Life Insurance Retirement Plan (LIRP) using cash value contracts shares some important advantages with a Roth IRA. But surely there are some differences, right?

1. Contribution limits. As mentioned earlier, "non-back-door" contributions to a Roth IRA are constrained by contribution limits, income ceilings that can completely phase out eligibility, and other plan requirements.

And the source of contributions has to be from "compensation" which usually translates to "earned income." If you're fortunate enough to be able to set up a maximum "back-door" IRA arrangement, the maximum annual contribution today is $38,500. Otherwise, the maximum annual amount is $6,000, or $7,000 for age 50 and above.

Alternatively, there are no limits on the amount of premium that you can pay into a life insurance contract, and no requirements as to the source of the funds. You can pay premiums from dividends, interest you earn, funds you have on hand, pension payments, whatever. And the Tax Code places no limits on the amount of life insurance you can buy, or the premiums you can pay.

2. Estate planning. In estate planning, Roth IRAs are always included as part of the estate. Roth funds are subject to both Federal and State estate and inheritance tax liability. Life insurance can be, and often is, structured so that the death benefit is not included in the value of the estate for tax purposes.

3. Investment choices. Roth IRAs offer more flexibility in investment choices than life insurance products, where the investment alternatives are limited to what the issuing insurance company chooses to offer. However, because of the insurance element in a life insurance contract, there is less potential for high volatility in a life insurance investment portfolio than in a portfolio consisting of exchange-traded securities.

4. Life insurance includes a death benefit. For income replacement, wealth creation, charitable endowments, you name it. Roth IRAs do not.

All of this means that, as always, there is both good news and not-so-good news.

The good news: There is an alternative to the "back-door mega-strategy" that can offer your clients many of the benefits that Peter Thiel enjoyed - and more. And, with your help, they can start using that strategy today.

The not-so-good news: Even with the flexibility and advantages of a LIRP, your clients probably won't be able to start with $1,664 and turn it into $5 billion in 20 years. C'est la vie.

So, why sneak around to the back door when the front door is wide open? As we said in our earlier Blog — An Idea That Keeps Getting Better, Stronger and Easier — today's financial environment is perfect for the products you know and sell. At Windsor, we know the products, the features, the companies and the underwriting that will fit your clients' needs and provide solutions and security for their future. Call us - we'll be happy to help with your client's life insurance and retirement income needs. There's no better time than right now!

Comments