The Real Costs of Waiting - Part Two

"Complicated [permanent life insurance] products eat away at the purchasing power of your premium. In most situations, your financial planning will be better served by buying term life insurance and then investing outside of the insurance contract.1

"Do not let anybody tell you that your life insurance policy is a good way to build extra savings. Fall for that and you will end up wasting thousands of dollars over the life of the policy.2

As life insurance professionals, we know that sentiments like those above are nothing new. And in response, Windsor's recent Blog — Life Insurance and Retirement Planning – A View From Outside the Industry — reviewed a report from Ernest & Young, LLP (EY), that extensively examined whether using life insurance cash values to supplement retirement income really made sense when compared with alternative investment strategies. Among EY's conclusions:

"Allocating up to 30% of annual savings to Personal Life Insurance . . . may be appropriate when optimizing retirement values and legacy value outcomes."

And –

"More exposure to Personal Life Insurance . . . produces better retirement outcomes because it does not result in an under-allocation to equity assets earlier in the household's life cycle."

And –

"Our analysis shows that integrating insurance products into a financial plan provides value to retirement investors."

Building on EY's report, we posted a subsequent Blog —The Real Costs of Waiting – Part One — where we discussed and analyzed the premium costs that come with health issues and underwriting rate class changes when clients choose to postpone the purchase of life insurance. The examples we cited were for a death benefit need, and the potential additional cost was significant. A similar analysis can be applied to sales where cash accumulation using personal life insurance, as EY's report recommends, is one of the primary goals of the client.

Our analysis revealed that for cash accumulation purposes, delaying a purchase by just a few years can impact both the required premium and income potential of a policy to the tune of several thousand dollars a year, or more. Let's look at a typical case to help illustrate these costs.

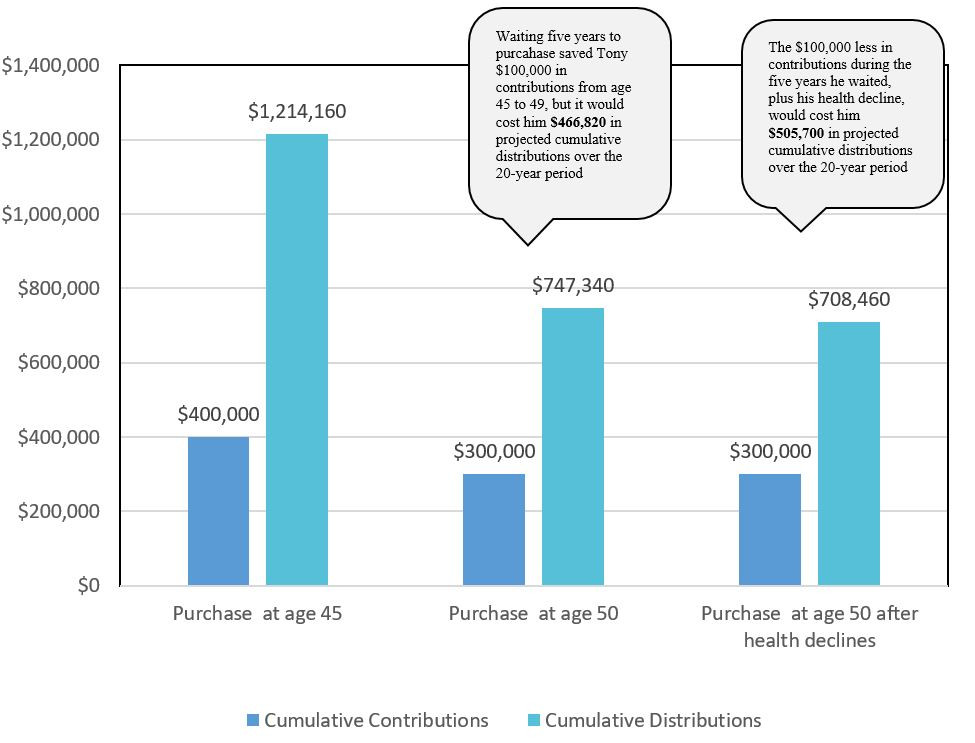

Tony is a healthy 45-year-old who owns a successful business. He has maxed out contributions to his qualified retirement plan, and is looking for additional ways to put away tax-advantaged dollars for retirement purposes.

During your meeting with Tony, you demonstrate how a cash-value life insurance product could perform assuming he contributed $20,000 a year for 20 years ($400,000 in cumulative contributions), with 20 years of distributions beginning at age 66 until age 85.

Tony currently qualifies for super preferred underwriting, and you recommend an Index Universal Life product, which you and Tony agree to review using a 6.25% illustrated interest rate.

The illustration shows 20 years of projected income of $60,708 annually starting at age 66 ($1,214,160 in cumulative distributions).

The Cost of Waiting

Example 1

If Tony decides to wait five years, delaying his purchase until age 50 along with distributions commencing at age 66 and using the same $20,000 premium funding pattern:

The product is now projected to generate only $37,367 annually, for a total cumulative distribution of $747,340.

Waiting just five years to begin his plan will cost Tony $466,820 in projected cumulative distributions over 20 years from age 66 to age 85.

Example 2

If Tony decides to wait five years, with distributions commencing at age 66 and using the same $20,000 premium funding pattern, AND his health declines where he now qualifies for only a standard underwriting class:

Under this scenario, Tony's product would produce only $35,423 per year. This represents a decrease of $505,700 in projected cumulative distributions over 20 years.

Example 3

Let's assume Tony decides to wait five years, and commencing at age 66 wants the same $60,708 distribution for 20 years he was projected to receive earlier.

Since the premium payment period is condensed to 15 years, Tony would need to pay $32,415 per year instead of the $20,000 he originally planned over a 20 year period. The total aggregate increase in premium is $86,225 — roughly a 22% increase.

If his health declines to a standard premium class, the premium would be $33,892. The total aggregate increase in premium is $108,380—a roughly 27% increase.

What could your client do with an extra $86,000 or $108,000?

Take the next steps…

If you have clients who are qualified candidates for permanent coverage but are hesitant to get started, show them these examples, or give us a call at Windsor for customized illustrations designed to suit your clients' needs. We can help you persuasively demonstrate the increased expenses and reduced benefits that add up to the real costs of waiting.

Comments